Best annuity quote

The annuity quotes were the best that I received.

Jackie Marsh

Turn your pension savings into guaranteed income, with no investment risk

An annuity is a way to turn money in your ‘defined contribution’ pension savings into guaranteed retirement income for life, or for a fixed term of your choice.

You will have peace of mind when it comes to your finances because there won’t be any unexpected changes to your income. That’s because it won’t be affected by changes to stock markets or interest rates - unlike other investment-based retirement income solutions.

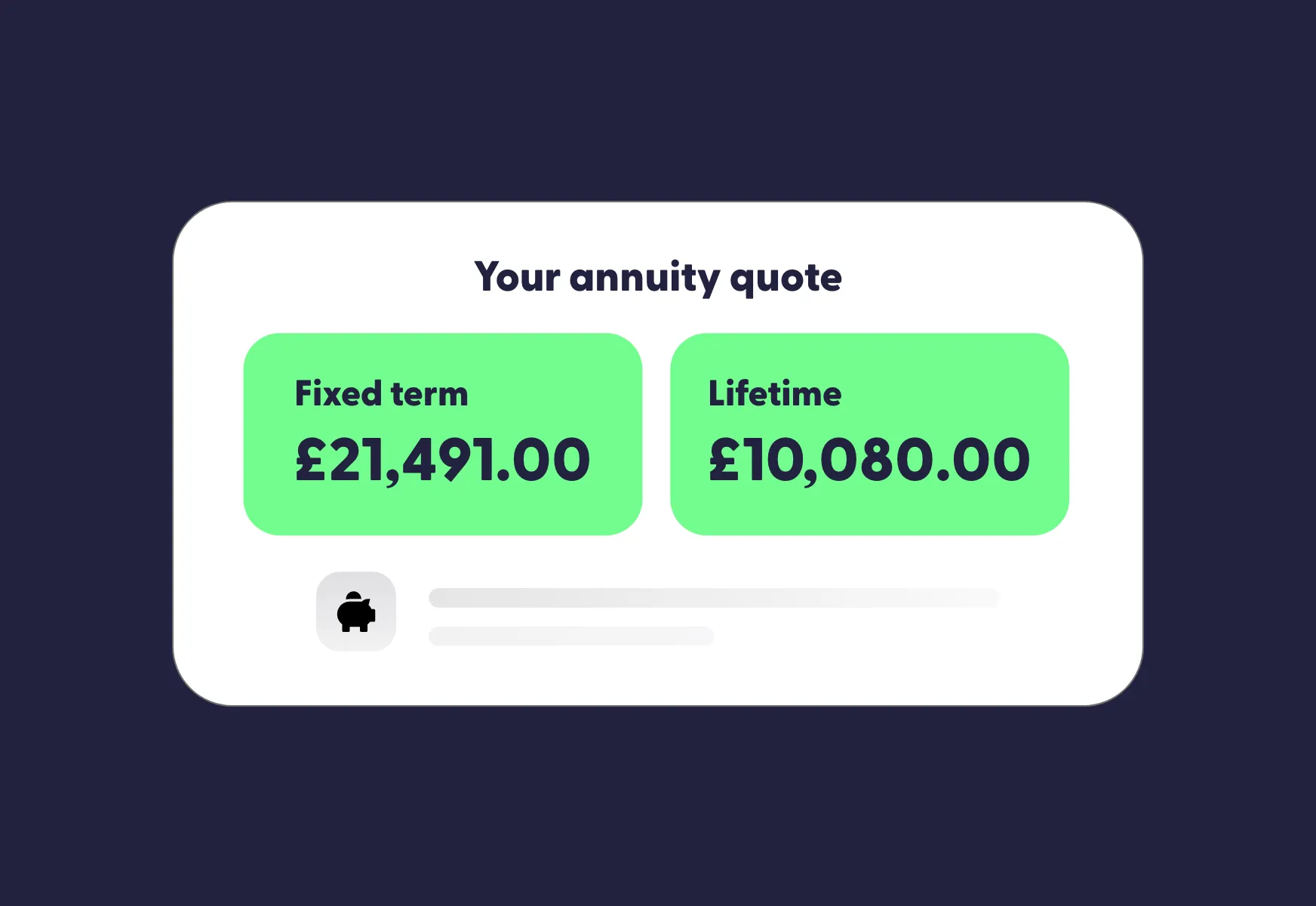

How much income you receive depends on the size of your pension pot, your age, the rate the annuity provider offers and whether you choose a lifetime or fixed-term annuity. Poorer health or lifestyle may also affect your income, potentially qualifying you for more with an enhanced annuity. Purchasing a pension annuity is something you can do from age 55 (rising to 57 from April 2028).

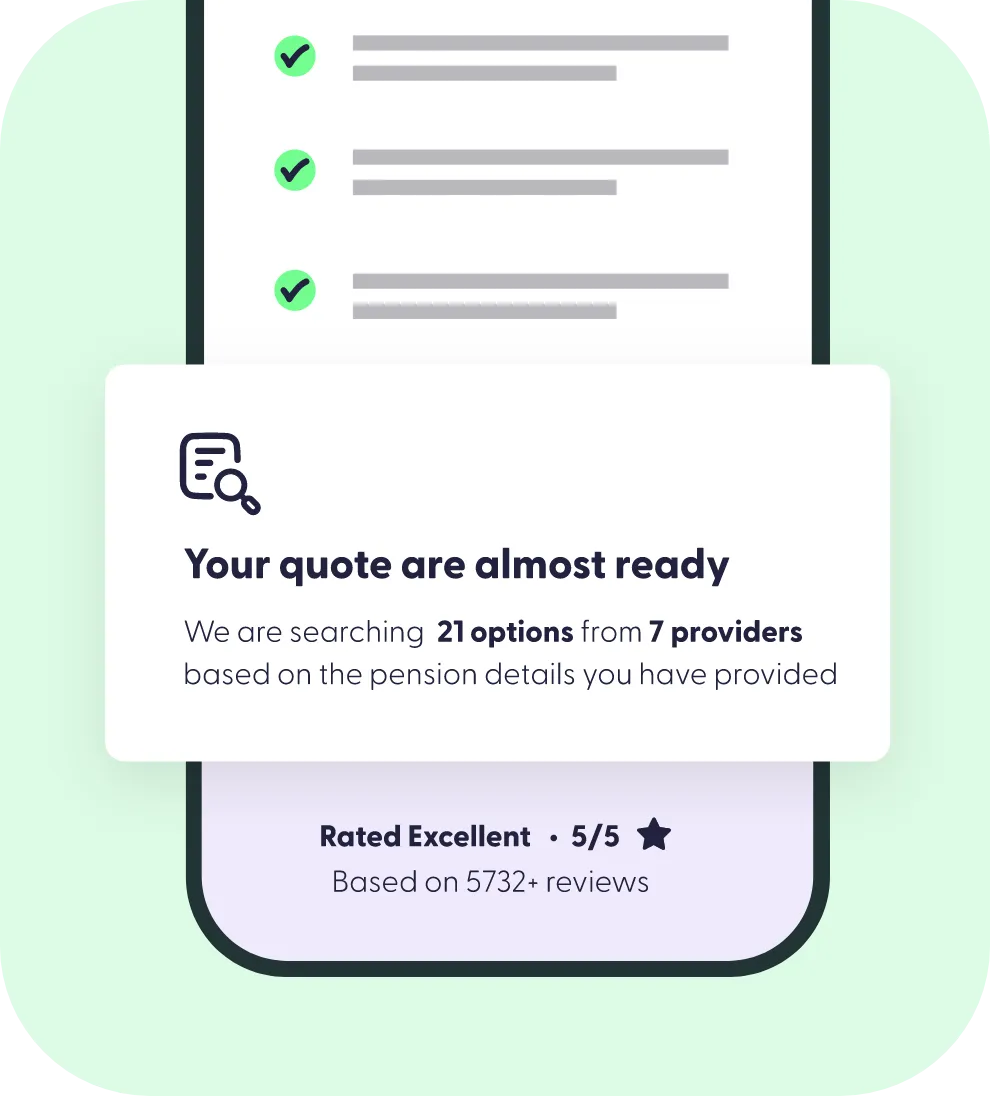

Annuity rates differ from provider to provider, so that means comparing rates and income levels from each one is crucial. It could add thousands of pounds to your pocket over the course of your retirement. Compare More’s selected annuity specialists will do this for you, ensuring you access the best available deal and guaranteed income.

The main attraction of annuities is that they deliver care-free guaranteed income. You’ll always know how much your annuity will pay, and you’ll never worry about stock market changes affecting your lifestyle.

With an annuity you have a secure level of income for life or a fixed term, allowing you to budget more accurately.

Once your annuity is set up, you have nothing else to do. There’s no need to monitor a pension fund or manage investments.

You could benefit from better rates and a higher income if you have qualifying medical conditions or lifestyle choices.

You can include benefits for your spouse or any nominated beneficiary on your death, either income or a lump sum.

Your income is locked in, no matter what happens to the stock market or interest rates. Complete peace of mind.

The cost of setting up your annuity is built into your annuity rate, so there are no ongoing management charges.

Setting up your retirement income is a big decision, so it’s good news that our annuity comparison partners enjoy great feedback and an ‘excellent’ Trustpilot rating from customers who have used the service.

The annuity quotes were the best that I received.

Jackie Marsh

Everything explained, all questions answered, multiple quotes from a range of providers covering all options.

John Cole

Would highly recommend this company for annuity purchase… a company you can trust.

Michael Greene

I couldn't have asked for a better service and would thoroughly recommend them.

Francis Adams

They took the time to understand what I was looking for, helping me select the best option without any pressure.

Graham Carter

Found the best annuity rate for my father, which was considerably more than the rates offered by his existing provider.

Alex Thomson

Explore your options to find an annuity that’s best for you.

See our guide to annuity rates for information on how they work, how they affect you, and the best rates currently available from UK providers.

At Compare More we gather quotes on your behalf from the UK’s leading annuity providers. To help us show you quotes to match your circumstances and needs, we need to know:

Your pension savings

The value of your pension fund will impact the income you receive from your annuity. We also ask whether you wish to take any tax-free cash before buying your annuity, as this also affects your income.

When do you plan to retire?

Your retirement date is when you want your annuity to start and should be within two years for the most accurate quote.

Your personal details

You’ll need to share details like your age, postcode, whether you smoke and if you have any medical conditions as these will affect your annuity income. We also need some contact details so we can get in touch with information about your quotes.

Comparing annuities is one of the best ways to make sure you are getting the biggest possible income from your pension savings. Before you dive in, it is worth thinking about your priorities and getting clear on your options. Here are a few tips to help you along the way:

Lifetime or fixed-term? You may want to look at illustrations for lifetime and fixed-term annuities to see which works best for you.

Think about what matters most to you: Do you want regular monthly payments, protection against inflation, or to leave something behind for loved ones? Knowing your priorities will help you find the right fit.

Be upfront about your health: It might feel a bit personal, but being honest about your health and lifestyle could mean a bigger income. Providers offer enhanced annuities to people with medical conditions or certain lifestyle factors.

Inflation factor: A level annuity might look attractive at first because it pays more upfront, but inflation can chip away at its value over time. An inflation-linked option could give you peace of mind for the longer term.

Get expert help: Buying an annuity is a big decision, so it is worth doing properly. An annuity specialist can compare rates for you and explain how the various products and features work.

Taking the time to shop around can make a huge difference to your retirement income. The key is making sure your choice lines up with your goals and needs for the years ahead.

“When buying an annuity, it’s crucial that you shop around for the best deal. Recent research found that the average gap between the lowest and highest income from annuity providers is 13% for 65-year-olds, and a staggering 20% for 70-year-olds. That means you could secure thousands of pounds in extra income by comparing annuities from the leading providers. ”

Guest Contributor, Pensions

Page updated on 27th July 2025, Reviewed by Richard Groom